Even with limited data due to COVID-19, an annual benchmarking report found that the operating margin for skilled nursing facilities remained at zero for 2019. And given the costs of managing operations during the pandemic — to say nothing of the occupancy hit — the picture is bleak for margins in 2020.

But for all the outside forces remaking the operating landscape, SNFs still have some control of their destiny, and they need to ensure they don’t overlook the fundamentals — such as optimizing revenue under the Patient-Driven Payment Model (PDPM), the Medicare overhaul that took effect just over a year ago, or managing their star ratings under the Nursing Home Compare system.

In other words, provides need to make sure they’re not losing track of the basics.

“We’ve found that in talking to organizations, it’s very easy to get overwhelmed with all of the COVID conversation, and understandably so,” Cory Rutledge, the principal who leads the senior living practice at professional services firm CLA, told Skilled Nursing News. “We’re just attempting to make the point that we also need to step back and take a look at the skilled nursing business and recognize that the metrics that have always been important continue to be important.”

CLA’s 35th SNF Cost Comparison and Industry Trends Report drew from annual SNF cost report data from the Centers for Medicare & Medicaid Services (CMS) for 2019.

In a typical year, the report would incorporate information from 12,000 of the roughly 14,000 reports filed, but 2020 has been far from typical; due to a pandemic-related cost report filing extension from CMS, approximately 6,000 cost reports were available for CLA’s analysis, Rutledge noted.

That said, some clear themes did emerge from the 2019 data. The operating margin remained around 0% for the third year in a row, and even though many operators saw increased reimbursement for Medicare patients under PDPM, the impact for 2019 was limited given the system’s start date of October 1, 2019.

The report also raises concerns, in an indirect way, for providers hoping to see some of those increases; in the 2019 data, the average Medicare mix declined by 90 basis points in SNFs, accounting for 9.4% of total days. Medicaid days stayed roughly flat, going from 61.9% on average in 2018 to 61.8% in 2019.

The proportion of other payers, including Medicare Advantage (MA), private pay and others, rose 1% from 2018 to 2019.

These changes can be attributed to several factors, according CLA, including:

- MA enrollment growth

- Lower hospitalizations

- Shorter lengths of stay in both the SNF and hospital settings

- Home health and outpatient therapy serving as care substitutes

“Medicare and many MA plans are implementing more value-based payment mechanisms, which highlight the need for facilities to monitor and improve quality metrics,” the report said.

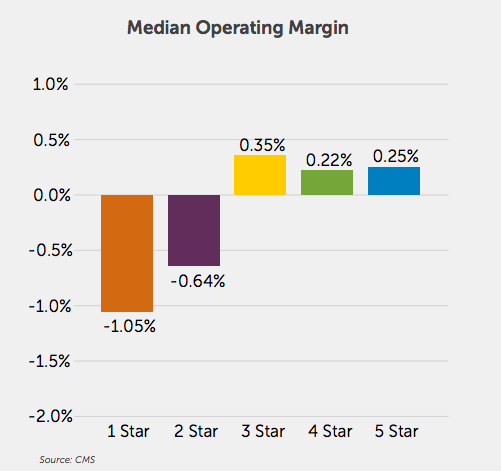

The data for last year also indicated a correlation of some kind between a facility’s star rating and its operating margin. In 2019, SNFs with an overall star rating of 1 or 2 had margins well below the median of zero; SNFs with ratings of 3 or higher had margins above it, though the effect was slightly less pronounced.

Star ratings also appeared to have some correlation to occupancy, according to the CLA report. The median occupancy rate for SNFs across the U.S. in 2019 was about 84.6%, but facilities with an overall rating of three stars or higher had occupancy either approximately equal to or above that number. Facilities with an overall rating of five stars had a median occupancy 87.8% last year, CLA found.

Census in SNFs has taken a beating this year amid the suspension of elective surgeries and COVID-19 outbreaks, and discharges to the setting have yet to see any kind of recovery, according to the consulting firm Avalere Health. That’s a trend that CLA identified as critical for 2020, alongside the increased cash burn that is, in some cases, forcing operators to rethink their new normal.

The lack of recovery in occupancy has led some operators to reconfigure their operating model with the assumption that “pre-COVID occupancy levels are simply not realistic,” according to CLA.

The situations where this is necessary wiill vary considerably by market, Rutledge told SNN. But operators can examine some metrics to determine whether they need to reset expectations around occupancy, and whether they can expect a return to pre-pandemic levels.

“The most basic is just the demographics of the local community. So the percentage of individuals that are 75-plus or 85-plus and the growth of that demographic in the coming years — that’d be the first place I would look,” Rutledge told SNN. “Second, I would look at the hospitals that are in the market area and understand their referral patterns. Home health, I think [is] a great thing to look at. Understand the percentage of hospital discharges that go to skilled nursing, the percent that go to home, the percent that go home with home health.”

He also recommended assessing the number of beds per thousand in population within a given market; a facility in an area that is overbedded would be “more ripe for a conversation around closure, or things of that nature.”

Because of the increased costs and declining occupancy, SNFs need to ensure that they aren’t making missteps on PDPM in terms of leaving money on the table, CLA emphasized.

It’s something early reports on the have raised as a possibility, and Rutledge emphasized that it’s factors such as this one, within the control of SNFs, that can make a major difference.

“Nursing cost, I think, is a good example where there are aspects of that that certainly are in control, right?” he said. “A SNF operator has an opportunity to manage the nursing hours per patient day. Now there’s also an aspect that could be somewhat out of control, if there’s hero pay or things of that nature … but there are still specific aspects that an operator has influence over.”